As the UK accelerates its transition to a low-carbon economy, hydrogen is emerging as a key pillar in the country’s energy strategy. With significant government backing and industry momentum, hydrogen projects are taking shape across the UK. However, navigating this complex and rapidly evolving landscape requires clear insights. This is where Olsights Eye provides a game-changing solution—offering a comprehensive, interactive map of hydrogen projects to support decision-makers, investors, and policymakers in identifying opportunities and understanding regional trends.

The State of Hydrogen Development in the UK

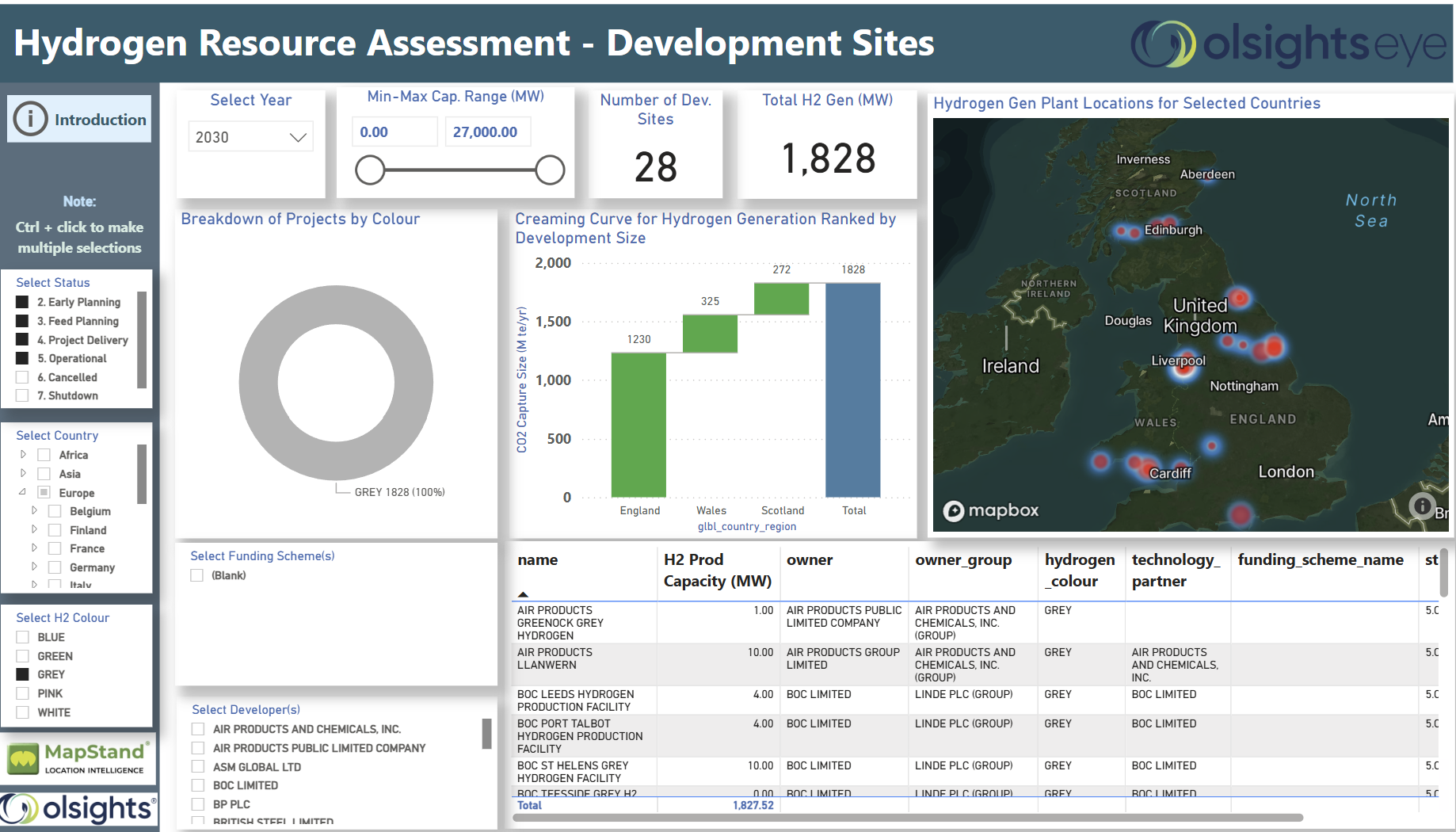

‘High Carbon’ Hydrogen Currently in Operation

Traditional hydrogen production remains dominated by grey hydrogen, which is derived from natural gas without carbon capture. Currently, the UK has 25 operational grey hydrogen sites with a combined capacity of 1,964 MW, with projections indicating 1,819 MW still in operation by 2030.

The Shift to Low-Carbon Hydrogen

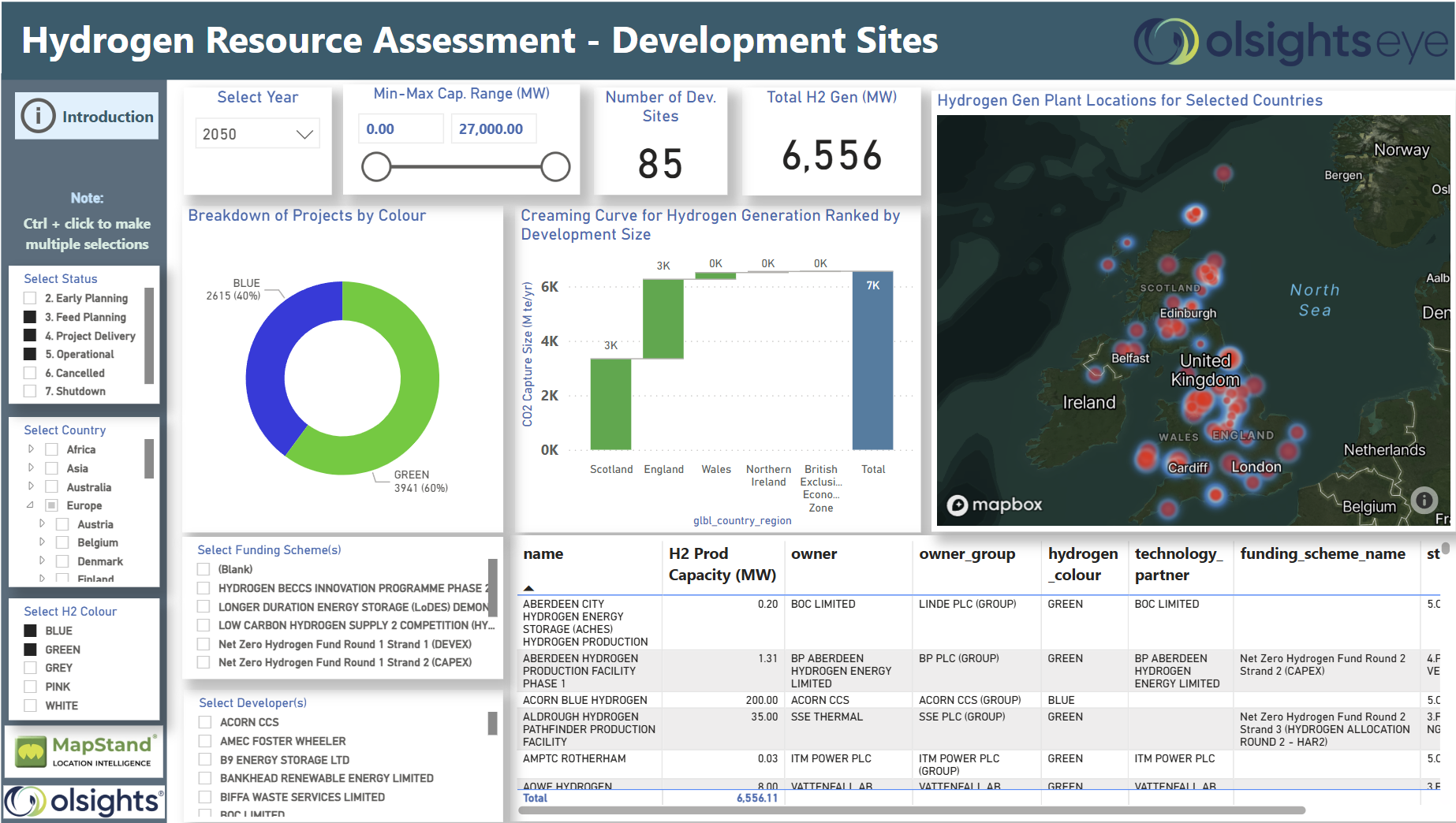

The UK’s drive toward decarbonisation is fostering rapid expansion in low-carbon hydrogen projects, which include both blue hydrogen (produced from natural gas with carbon capture) and green hydrogen (produced using renewable energy and electrolysis).

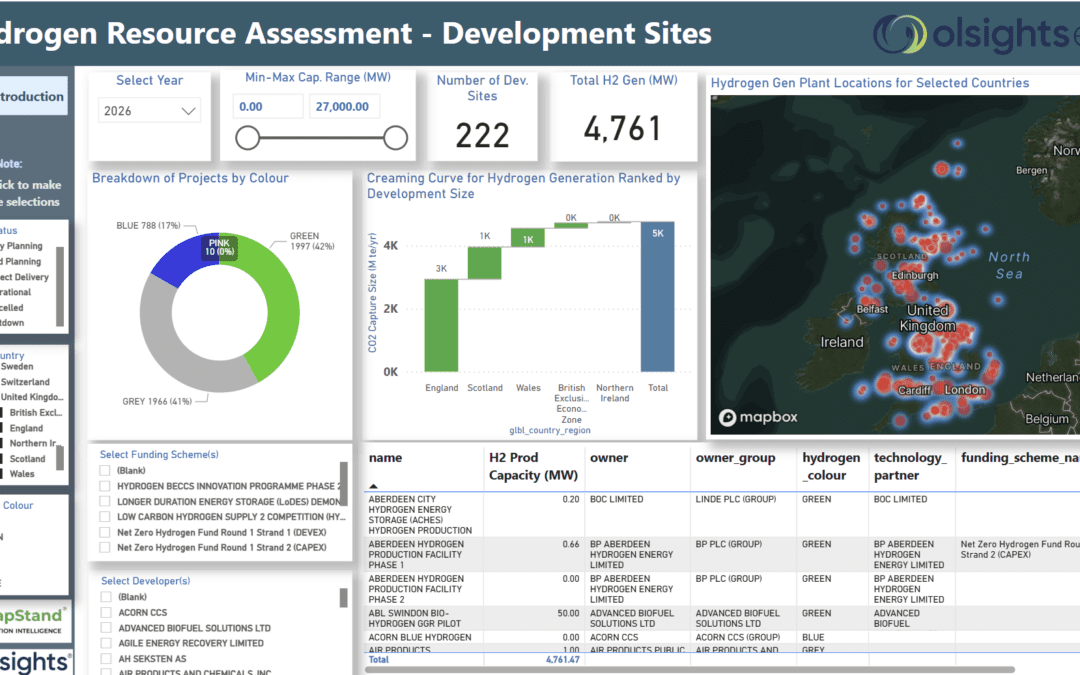

- Total low-carbon hydrogen projects in FEED, delivery, or operation by 2050: 85 sites, 6,556 MW (with 5,190 MW targeted by 2030)

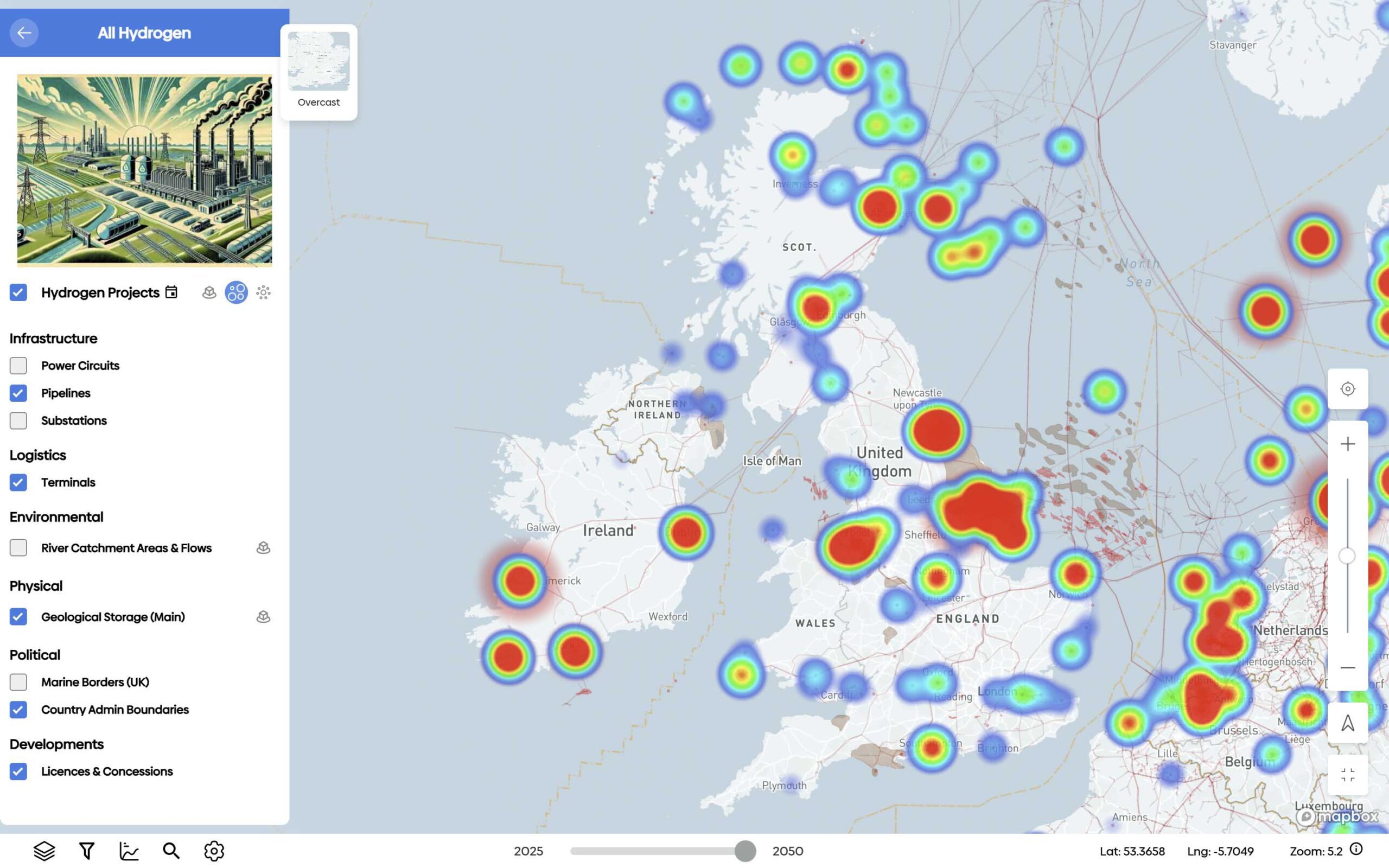

- Green Hydrogen: 74 sites, 3,967 MW (with 2,675 MW by 2030), dispersed across the UK but with over two-thirds concentrated in Scotland.

- Blue Hydrogen: 9 sites, 2,615 MW (with 2,515 MW by 2030), primarily in Teesside and Merseyside.

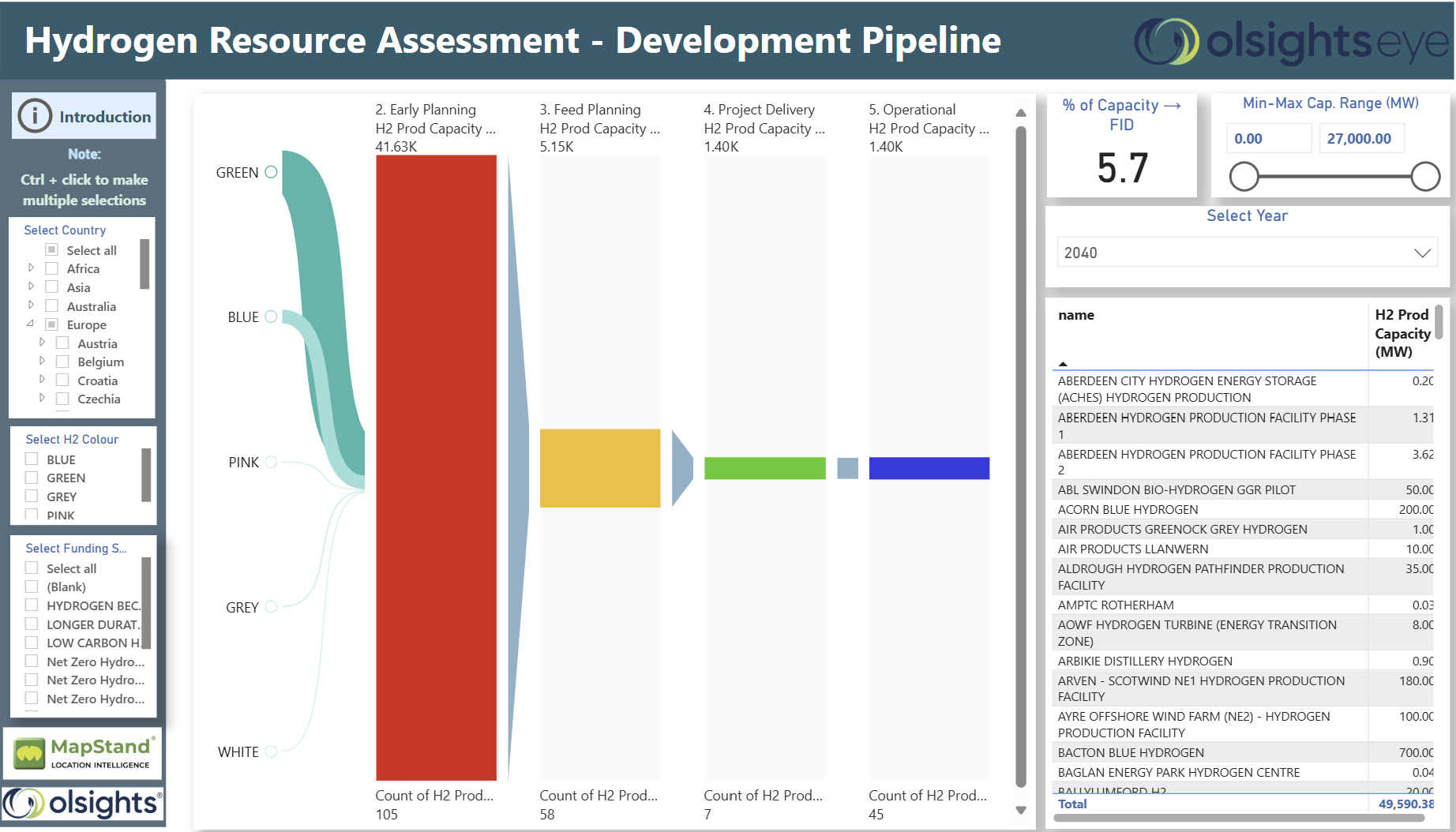

Scaling Up: Hydrogen Projects in Early Development

Looking beyond immediate developments, early-stage hydrogen projects signal significant future capacity. If these projects reach commercialisation, the UK could become a global hydrogen powerhouse.

- Total early-stage projects: 185 sites, 47,998 MW (with 19,090 MW by 2030)

- Green Hydrogen: 161 sites, 36,334 MW (with 9,335 MW by 2030), largely driven by Haldane (Bute)’s developments in Yorkshire and Cheshire’s salt cavern storage areas.

- Blue Hydrogen: 24 sites, 11,665 MW (with 9,755 MW by 2030), concentrated in Humberside, Teesside, and Merseyside.

Funded Hydrogen Projects: Near-Term Commitments

A subset of these projects has already secured funding, marking a significant step towards implementation.

- Projects in FEED (Front-End Engineering Design): 36 sites, 4,754 MW (with 3,512 MW targeted by 2030)

- Projects in Delivery: 2 sites, 1,201 MW, both aiming for completion by 2030

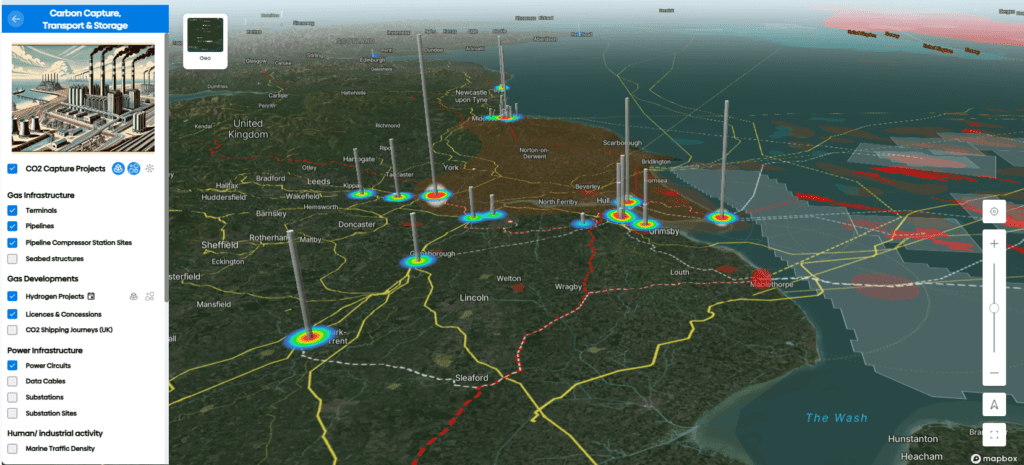

How Olsights Eye Supports Hydrogen Development

Understanding the geographical distribution and status of hydrogen projects is essential for efficient planning, investment, and policy-making. Olsights Eye provides a visual and data-driven platform that maps out hydrogen projects, enabling stakeholders to:

- Identify hotspots for hydrogen development: Quickly locate clusters of green and blue hydrogen projects, including their expected capacity and timelines.

- Track project progress: Gain real-time insights into projects in feasibility, FEED, construction, or operational stages.

- Assess regional infrastructure readiness: Understand where hydrogen production aligns with existing energy networks, storage, and transportation corridors.

- Support investment and policy decisions: Provide data-backed insights to help guide funding allocation and strategic partnerships.

Conclusion

The UK’s hydrogen landscape is evolving rapidly, with ambitious targets for decarbonisation and industrial growth. However, success depends on clear insights and efficient decision-making. With the Olsights Eye, stakeholders can cut through complexity, access real-time project data, and map the future of hydrogen with confidence.

Contact us for a full demo of the Olsights Eye for more details – hello@olsights.com