Why Understanding Future Constraints May Matter More Than Running the Tender

The UK’s flexibility market has matured rapidly over the last decade.

Distribution System Operators (DSOs) have embraced flexibility as a critical tool for managing network constraints, reducing reinforcement costs and enabling the transition to a low-carbon energy system. Market Procurement Organisations (MPOs) have developed sophisticated procurement platforms, aggregators have expanded their portfolios, and regulatory frameworks continue to evolve.

Yet despite this progress, a fundamental challenge remains largely unresolved.

How do we identify where flexibility will be needed before procurement begins?

As the industry prepares for RIIO-ED3, the answer to this question could prove just as important as the procurement process itself.

At Olsights, we believe the next stage of flexibility market maturity will be driven not by better auctions, but by better intelligence.

The Industry Has Built Procurement Infrastructure

Now It Needs Intelligence Infrastructure

Today’s flexibility ecosystem is increasingly effective at procuring services once a requirement has been identified.

However, procurement is only the final step in a much longer decision-making process.

Before any flexibility tender is launched, network operators must understand:

- Where constraints are likely to emerge

- How severe those constraints may become

- Whether flexibility offers better value than traditional reinforcement

- Which assets are best positioned to respond

- When procurement activity should begin

Answering these questions requires combining multiple complex datasets, including:

- Distribution Future Energy Scenarios (DFES)

- Network Development Plans (NDPs)

- Constraint assessments

- Reinforcement programmes

- Connection queues

- Demand growth forecasts

- Distributed generation pipelines

- Historical flexibility procurement data

The challenge is not a lack of information.

The challenge is transforming fragmented information into actionable intelligence.

This is precisely where Olsights has focused its efforts.

For several years, Olsights has been helping organisations understand complex energy systems through advanced data visualisation, geospatial analytics and decision-support tools. Through Olsights Eye, stakeholders can explore large-scale energy datasets in a way that enables faster, more informed decision making.

As flexibility markets evolve, we believe these capabilities have an increasingly important role to play.

The Emerging Governance Challenge

Recent developments across the flexibility sector have highlighted another important consideration.

The acquisition of Rhythmos by Electron was widely viewed as a logical expansion of flexibility market capabilities, combining EV flexibility analytics with market platform operations.

However, it also raises an interesting strategic question.

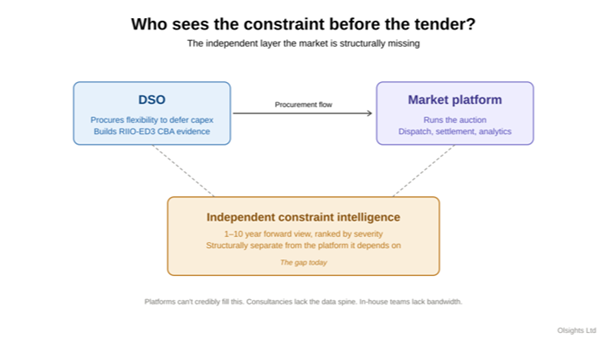

If the organisation operating the flexibility marketplace is also responsible for developing the intelligence that identifies future procurement opportunities, who provides the independent assessment of whether procurement is required in the first place?

This is not a criticism of market platform operators.

Rather, it reflects a structural challenge that naturally emerges as markets mature.

Market facilitators are designed to support procurement activity. Their incentives are aligned towards enabling successful tenders and efficient market operation.

The independent assessment of future network constraints, commercial viability and long-term flexibility opportunities requires a different perspective.

As RIIO-ED3 approaches, this distinction is likely to become increasingly important.

Figure 1: The emerging gap between procurement activity and independent constraint intelligence.

The Visibility Problem Facing Flexibility Service Providers

The implications extend beyond network operators.

Today, many Flexibility Service Providers (FSPs) are making strategic decisions about their portfolios based on limited historical procurement data.

Most organisations have access to only a handful of procurement cycles from which to forecast future revenues.

Yet the decisions being made today will influence investment strategies through to 2030 and beyond.

There are plausible scenarios where local flexibility services become a major component of FSP revenue streams.

There are equally plausible scenarios where activity remains concentrated within a relatively small number of established flexibility zones.

The difference between these outcomes may depend on visibility.

Those organisations that can identify emerging flexibility opportunities earlier than competitors will be better positioned to secure assets, develop customer relationships and build commercially attractive portfolios.

The challenge is that the market currently provides very few forward-looking signals.

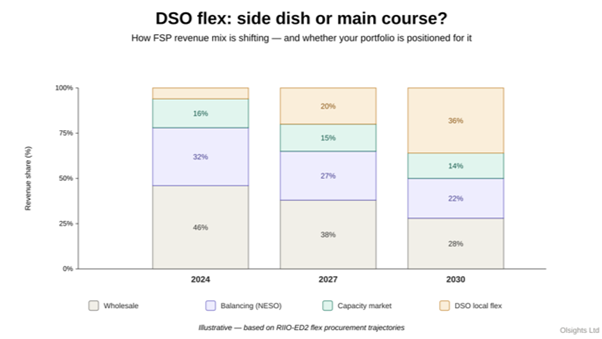

Figure 2: Illustrative scenario showing how DSO flexibility could become a larger proportion of FSP revenues by 2030.

The Hidden Cost of Finding Opportunity

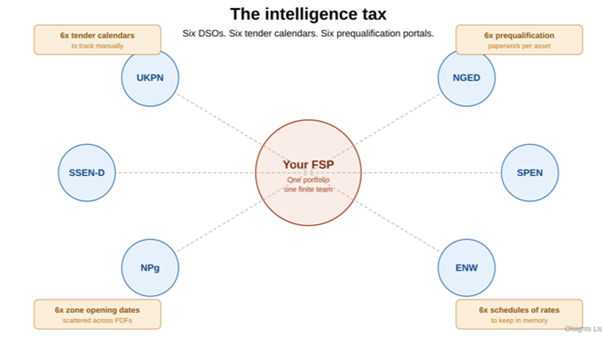

The UK’s flexibility landscape remains highly fragmented.

Six DSOs operate six procurement programmes, six publication schedules and multiple channels for communicating market opportunities.

Information is dispersed across:

- Flexibility portals

- Stakeholder webinars

- DFES reports

- Network development plans

- Consultation documents

- Procurement announcements

For national aggregators, monitoring this information has become a significant operational burden.

Industry discussions suggest some organisations dedicate the equivalent of one or two full-time employees simply to tracking emerging opportunities across multiple DSO territories.

While the staffing cost is manageable, the opportunity cost is much larger.

Missed procurement windows, delayed asset deployment and poor visibility of future market opportunities can significantly impact commercial performance.

This is not fundamentally a data problem.

It is an intelligence problem.

Figure 3: Flexibility Service Providers often spend significant effort monitoring multiple DSO processes and procurement channels.

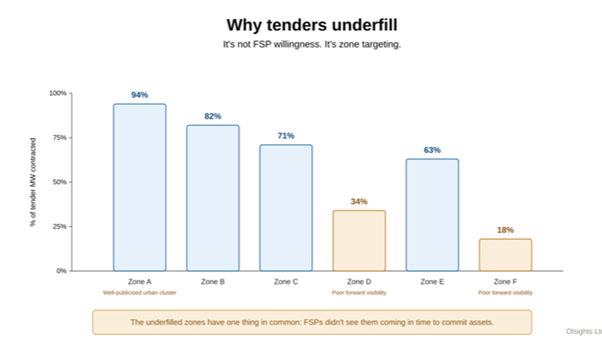

What Recent Procurement Performance Tells Us

Analysis of recent flexibility procurement rounds reveals a consistent pattern.

Some flexibility zones regularly contract 80–95% of their tendered capacity.

Others repeatedly achieve significantly lower utilisation rates.

Importantly, these underperforming zones are not concentrated within a particular geography or network operator.

Nor is there evidence that aggregators have lost interest in participating.

Instead, many underfilled tenders appear to share a common characteristic.

Market participants simply did not have sufficient visibility far enough in advance to prepare assets and develop participation strategies.

In other words, many of the challenges associated with underfilled flexibility tenders may be symptoms of poor forecasting rather than poor market design.

Figure 4: Underfilled flexibility tenders are often linked to poor forward visibility rather than lack of market interest.

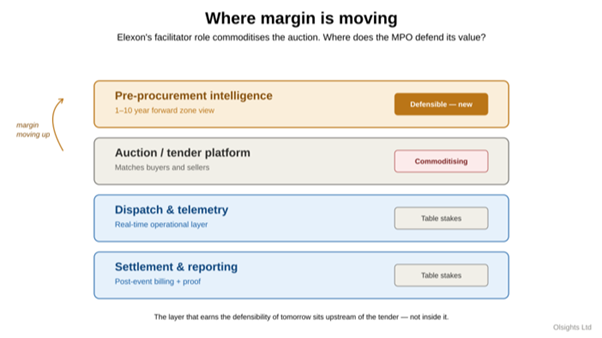

Why Constraint Intelligence May Become the Most Valuable Asset

As Elexon’s role in flexibility market governance continues to evolve, many MPOs are beginning to ask an important strategic question.

Where does long-term competitive advantage come from?

The auction layer itself is becoming increasingly standardised.

Tender management, market clearing and procurement administration are all activities that naturally move towards efficiency and consistency as markets mature.

The greatest opportunity for differentiation may therefore sit elsewhere.

It may sit within the intelligence layer that informs procurement decisions before the tender process even begins.

Understanding:

- Where future constraints will emerge

- Which zones are commercially viable

- When procurement should occur

- Which assets are most likely to participate

could become significantly more valuable than the procurement mechanism itself.

Figure 5: As flexibility markets mature, value creation may shift from auction operation towards pre-procurement intelligence.

How Olsights is Building the Missing Layer

This challenge is one of the reasons Olsights has been collaborating with Energy Systems Catapult through the GridFlex programme.

Together, we have been exploring how advanced analytics and visualisation can help create a forward-looking view of flexibility opportunity across Great Britain.

Olsights is not starting from a blank sheet of paper. Through REACT, a Spatial Decision Intelligence Platform developed with SSEN Transmission and MapStand through the Ofgem Strategic Innovation Fund, we have already demonstrated how fragmented infrastructure data can be transformed into actionable planning intelligence. REACT combines network, generation, storage and policy datasets within a single decision environment, enabling planners to understand not only where capacity exists today, but where it is most likely to materialise in the future.

REACT already provides many of the capabilities required to build this intelligence layer, including:

- Integration of network, generation, storage and policy data

- Risk-based scoring using the Inevitability Index

- Movement from nameplate capacity to expected capacity forecasting

- Scenario-based infrastructure planning

- Identification of reinforcement priorities

- Transparent visibility of constraints, opportunities and trade-offs

- Strategic decision support for planners, developers and network operators

Most importantly, this intelligence layer is designed to sit above the procurement process.

It is independent of specific MPOs, independent of procurement methodologies and focused entirely on helping stakeholders make better decisions.

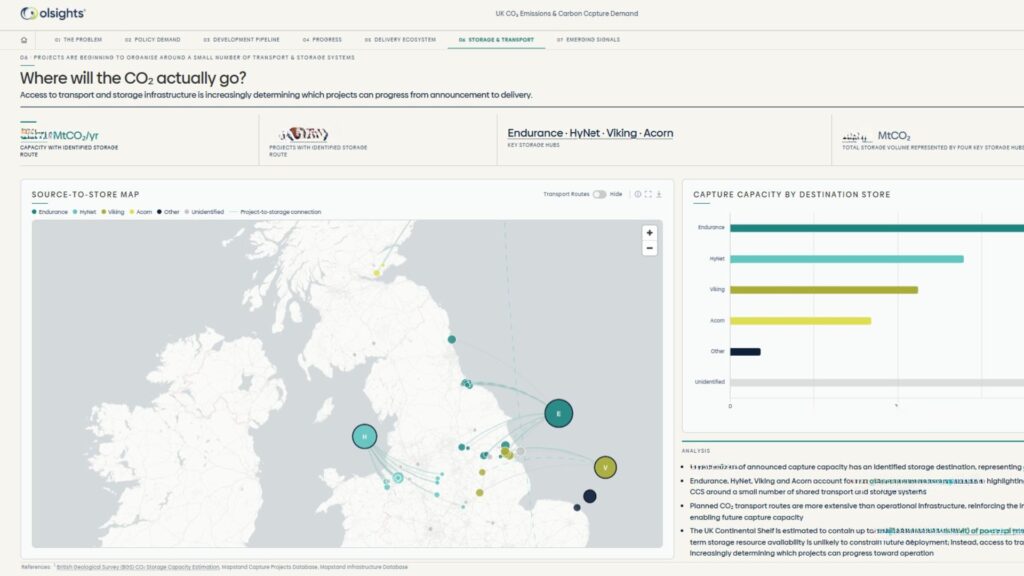

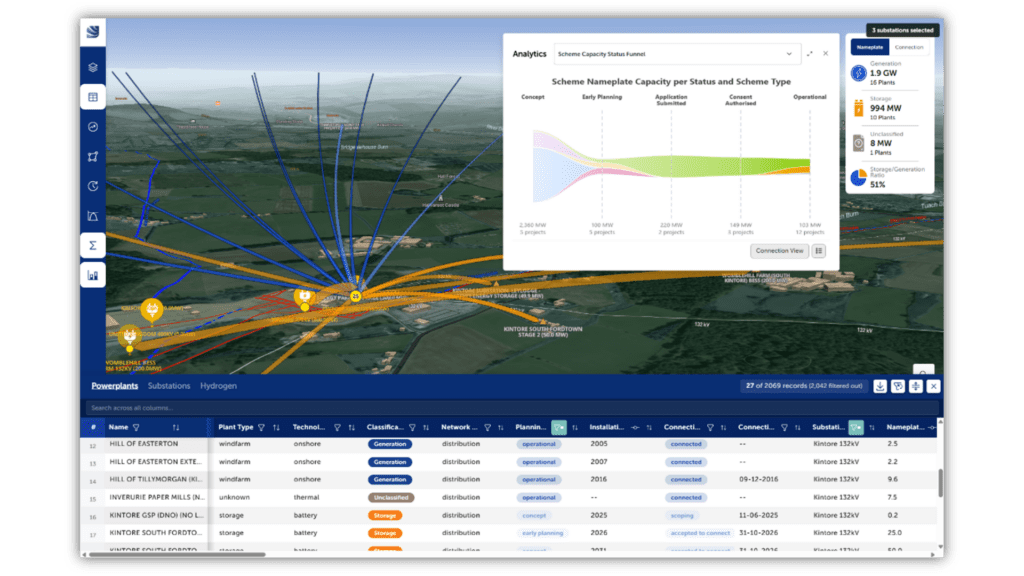

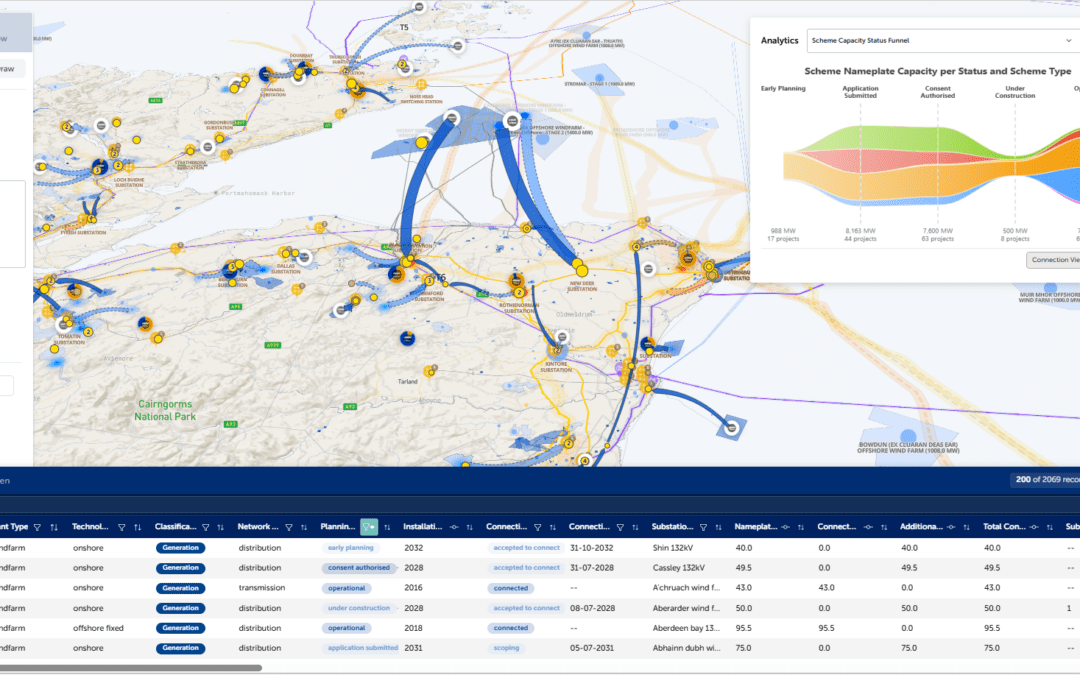

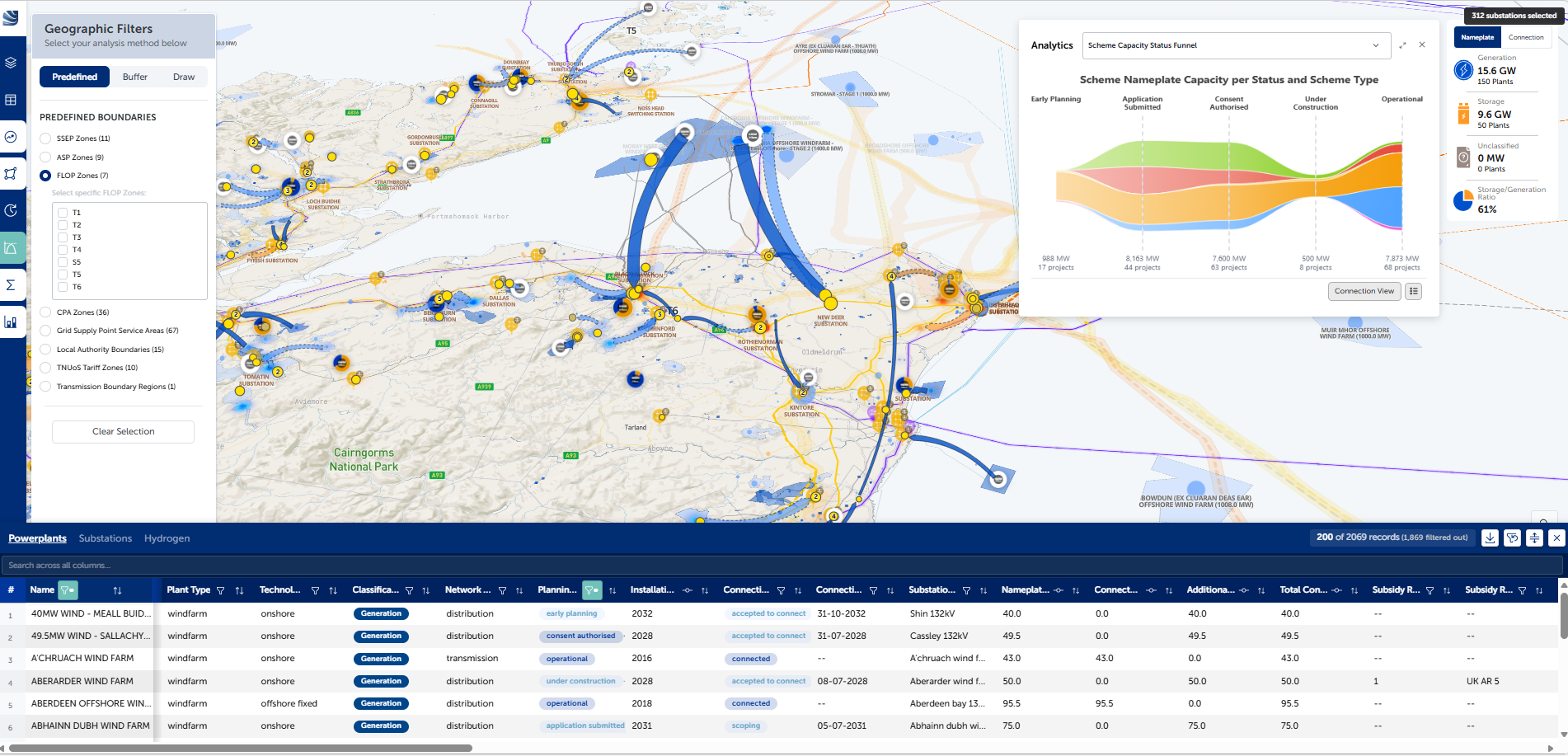

Figure 6: Screenshot of REACT. A tool created by Olsights in collaboration with MapStand and SSEN Transmission

Through Olsights Eye, stakeholders can already visualise network infrastructure, connection pipelines, capacity constraints and market opportunities within a single geospatial environment. By combining complex datasets into a single decision-support platform, Olsights Eye enables faster and more informed infrastructure planning. The lessons learned through REACT are now helping shape how similar intelligence can be applied to flexibility markets, creating a more connected view of future constraints, infrastructure investment and commercial opportunity.

From Complex Data to Strategic Insight

The energy transition is generating unprecedented volumes of data.

The organisations that succeed will not necessarily be those with access to the most information.

They will be those capable of transforming information into insight.

This is where Olsights is already delivering value through platforms such as Olsights Eye and innovation programmes such as REACT.

Through platforms such as Olsights Eye and methodologies developed through REACT, Olsights combines network infrastructure data, generation and storage pipelines, connection queues, policy drivers and market intelligence into a single spatial decision-support environment. This enables stakeholders to identify future constraints, assess likely project delivery, understand regional capacity build-up and evaluate flexibility opportunities with greater confidence.

Whether supporting network operators, flexibility service providers, infrastructure developers or policymakers, our goal remains the same:

Make complex energy systems easier to understand and easier to act upon.

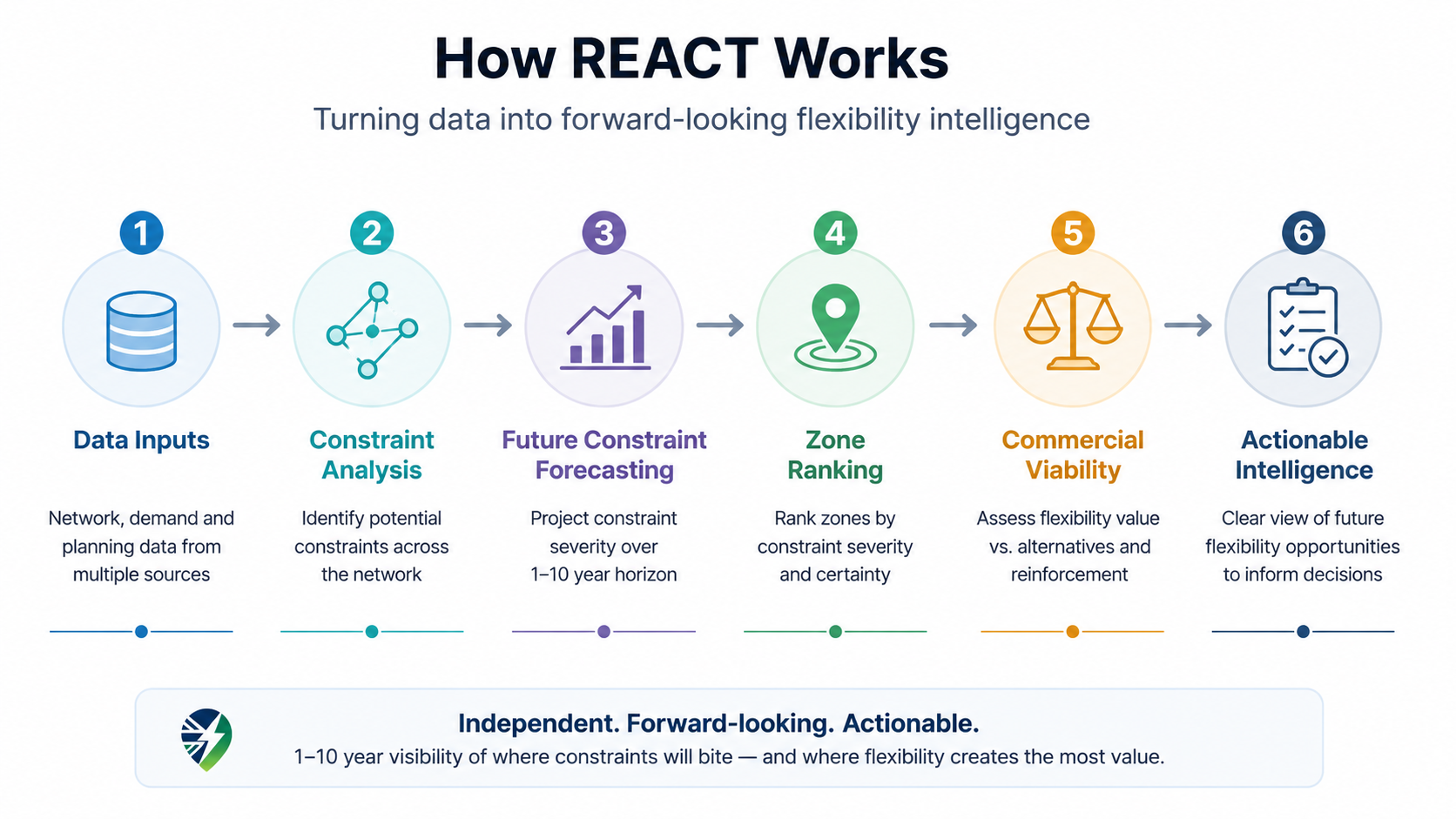

Figure 7: REACT Framework

Beyond Constraint Forecasting

While flexibility forecasting is one application of the REACT methodology, the underlying capability extends much further.

By integrating network, generation, storage and policy datasets into a single spatial intelligence environment, REACT enables stakeholders to move beyond static analysis and towards real-time, scenario-driven decision-making. It provides visibility not only of where constraints may emerge, but also which projects are most likely to connect, where network capacity is likely to materialise and where investment decisions can deliver the greatest impact.

This approach allows decision-makers to move beyond simple nameplate capacity assessments towards a more realistic understanding of expected capacity, helping prioritise investment, improve network planning and reduce the risk of inefficient or premature reinforcement.

Early evidence has shown that REACT has the potential to deliver more than £260 million of net benefit to UK consumers through improved targeting of network reinforcement, more efficient infrastructure investment and better-informed planning decisions.

Looking Ahead to RIIO-ED3

The flexibility market has invested heavily in procurement infrastructure over the last decade.

The next phase of market evolution may require a similar investment in intelligence infrastructure.

As networks become more complex and flexibility becomes increasingly central to the energy transition, the ability to forecast where flexibility will be needed could become a critical strategic capability.

Those who can see future constraints before they emerge will be better positioned to invest, participate and deliver value.

The market has spent the last decade building procurement infrastructure. The next decade will be defined by intelligence infrastructure. Through Olsights Eye, REACT and our collaboration with Energy Systems Catapult, Olsights is helping shape that future by providing the independent, evidence-based intelligence needed to understand where constraints will emerge, where flexibility creates value and where investment decisions will have the greatest impact. As RIIO-ED3 approaches, the organisations that can see further ahead will be best placed to capture the opportunities ahead. Through REACT, Olsights Eye and our ongoing work with industry partners, Olsights is helping define what that future intelligence infrastructure looks like.

References

- Ofgem RIIO-ED2 Final Determinations

- Energy Systems Catapult GridFlex Programme

- Energy Networks Association Open Networks Programme

- Elexon Flexibility Market Facilitator Programme

- National Energy System Operator Future Energy Scenarios (FES)

- Distribution Future Energy Scenarios (DFES)

- Ofgem Strategic Innovation Fund (SIF)

- REACT Network Innovation Allowance (NIA) Programme

- Olsights Eye Platform

- REACT Spatial Decision Intelligence Platform

This article is based on a series of LinkedIn thought leadership posts by Emmanuel Kirunda Olsights COO & Commercial Director