This weekend, I read the Deloitte 2023 Hydrogen report ‘Hydrogen – Making it happen’ and here are my main takeaways :

1. Deloitte’s decision to structure the discussion about hydrogen under 5 main topics ‘The 5 Factor Conditions’ is a good tactic to summarise the main aspects for scaling green hydrogen:

o Natural demand – the first priority to proliferate green hydrogen usage should be to roll it out in those sectors that are already using grey hydrogen, sectors such as refineries, chemical industry, etc.

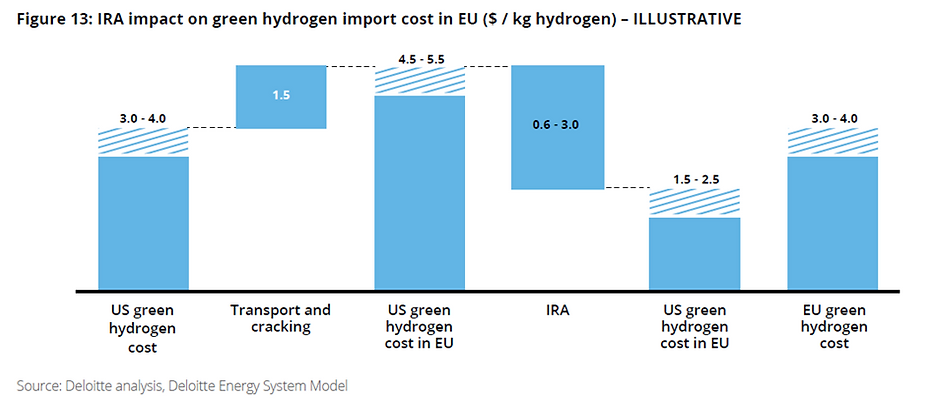

o Regulations – are key to spur both demand and supply. The examples of the US juggernaut regulation the IRA and the EU’s RED III are highlighted. The US IRA has greatly distorted the green H2 market with its up to $3/kg subsidy, which creates a condition where it is more economical for EU companies to produce hydrogen in US and import back to the EU (see graph below).

o Technology – Sectors that have clear decarbonisation pathways and mature technologies should adopt clean hydrogen faster. Those without should collaborate or invest more in R&D (to solve their challenges and create demand)

o Assets Infrastructure and supply – it is very insightful to know that switching over to H2 is inhibited by long asset replacement cycles for some industries. At best case, it takes decades to change them over to clean hydrogen. For example, steel has a lifecycle of 40 years, with 5% annual operational replacement, it would take up to 2065 if replacements starts in 2025.

o Collaboration – this is key for green hydrogen to reach scale. This can be achieved through the ideas of regional hubs and clusters which pool resources & reduce costs for production to enable economies of scale , and also allow large enough industry clusters as off-takers. Deloitte study of ‘the business case for hubs’ found that partnerships as part of a hub can save business as much as 95% of infrastructure costs as opposed to investing alone to achieve the same production volumes and emissions reduction.

2. Red flag: planned hydrogen projects need to be tripled between now and 2030. As of Aug 2022, 44Mt of new green hydrogen production and 9 Mt blue hydrogen production projects had been announced. According to IEA’s ‘Net zero by 2050 scenario , these figures must be tripled by 2030 to 150Mt in order to keep track with net zero. It doesn’t help that only 1% have passed FID (the biggest being China’s Xinjiang Kuqa project for 300 MW and Hollands’ 1 Holland Hydrogen 1 project 200MW). 80% of announced projects are less than 100 kt p.a capacity, with the two above mentioned biggest post-FID projects each being a mere 20 kt/yr. We need a 20 fold increase by 2030 of project approval, to keep pace.

3. Supply side investments for green electricity need to increase. In 2030 we need 80 TW of wind & solar renewable power, which is 8 times what it is now, and 4 times compared to the combined operational & what is planned.

4. Something new I learnt was about the Sustainable Aviation Fuels (SAF). Creative ways to spur SAF demand in Aviation include the Book and Claim Certification process. This process helps match demand and supply for SAF. Airline A pays premium for SAF, but uses normal fuel due to no supply, while Airline B in area with supply uses SAF but pays normal fuel price. Airline B does not get decarbonisation benefits, only A gets them.

5. The last takeaway was that more important than collaboration is the need for new commercial, business and risk models that can address the systematic issues that delay investments. That is in line with what we do at Olsights LTD. Our purpose is 100% about streamlining business and project processes, so that project initiation planning (both technical and economical) is expedited. Not only does this accelerate net-zero adoption, it also saves resources that would have been spent on non-economical projects. Check out our free web-app www.olsightseye.com that uses visualisations to accelerate how decision-makers gain insights regarding global decarbonisation projects.

By Emmanuel Kirunda