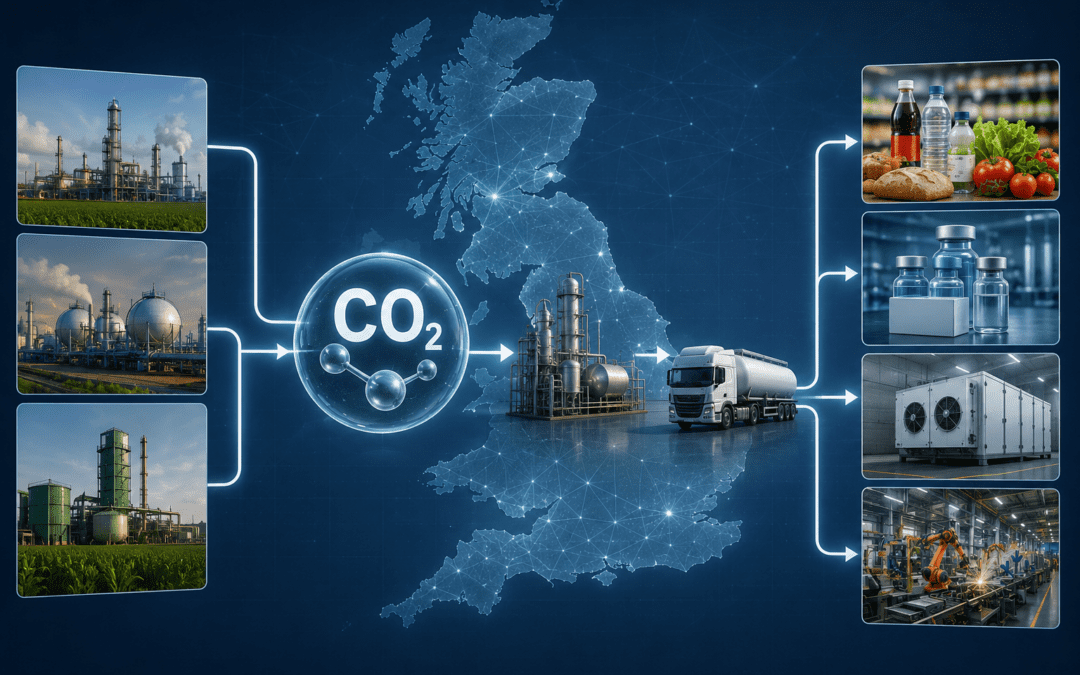

Commercial CO2 supply is rarely discussed outside industrial circles, yet it underpins critical sectors across the UK economy, from food production and healthcare to manufacturing and emerging carbon capture technologies.

Earlier this year, rising tensions between the US, Israel and Iran led to the closure of the Strait of Hormuz, triggering global fears over oil prices, energy security, shipping disruptions and wider supply-chain instability. These concerns emerged against the backdrop of an already fragile global energy market, still adjusting to the long-term implications of Russia’s invasion of Ukraine. However, this year, alongside these familiar concerns, an overlooked vulnerability became visible: a potential carbon dioxide (CO2) shortage.

CO2 is usually framed as a climate liability to be reduced or eliminated, yet modern industrial systems also depend heavily on stable supplies of commercial-grade CO₂ for food production, healthcare, refrigeration and manufacturing.

Whilst largely invisible to consumers, commercial CO₂ underpins a surprisingly wide range of industrial processes across food production, healthcare, refrigeration and manufacturing.

In most of these sectors, uninterrupted commercial-grade CO2 is operationally necessary, and this recent disruption across gas and fertiliser markets exposed how dependent UK food, healthcare and industrial systems remain on uninterrupted commercial CO₂ supply.

So what is the connection between geopolitical instability in the Middle East and the UK’s food & drink and healthcare sector operations?

The Structural Vulnerability Within Commercial CO₂ Supply

The answer lies in how the commercial carbon dioxide supply chain is structured.

Most usable commercial CO2 is not typically produced as a primary product, but rather as a by-product of ammonia, fertiliser and bioethanol production. Before it can be used within food or healthcare settings, it must also be captured, purified, liquefied and distributed through dedicated infrastructure.

This creates a structural vulnerability meaning that even countries with large industrial emissions can still experience shortages of usable commercial CO2 if disruption spreads across global gas and fertiliser markets.

That vulnerability became increasingly visible during recent geopolitical tensions, when UK media outlets warned of potential shortages affecting supermarkets, food manufacturing and industrial supply chains.

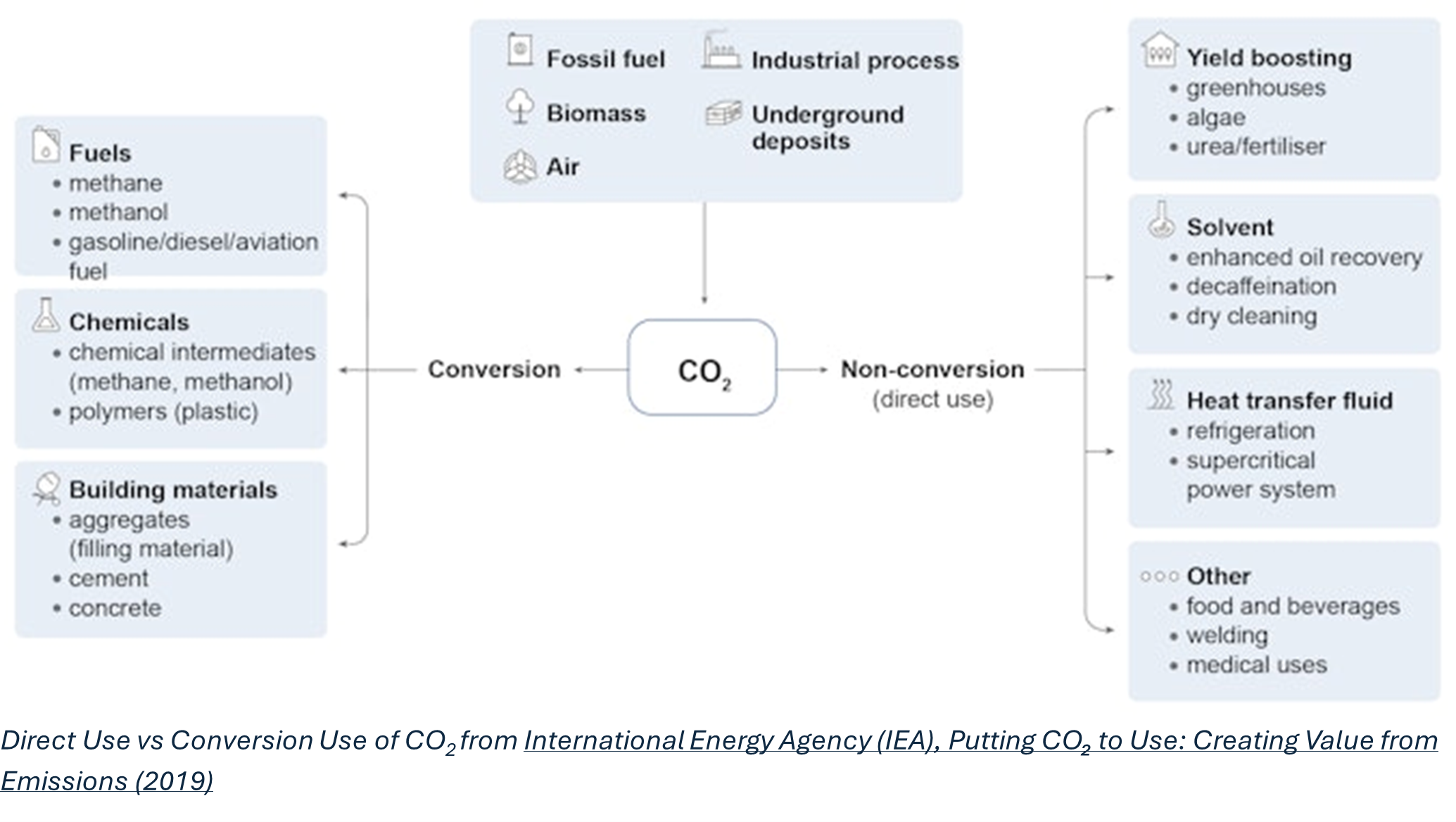

The broader importance of commercial CO₂ becomes clearer when examining global utilisation patterns. In a 2019 report, the International Energy Agency (IEA) estimated that approximately 230 million tonnes (Mt) of CO₂ were utilised globally each year. Fertiliser production accounted for the largest share through urea manufacturing (around 130 MtCO₂ or 57%), followed by enhanced oil recovery operations within the energy sector (at approximately 70 to 80 MtCO₂, or 34%).

Although food and beverage applications represent a relatively small share of global CO₂ utilisation, they remain highly sensitive to disruption because of their direct integration within food manufacturing, packaging and refrigerated logistics systems.

Beyond traditional applications, CO₂ demand is also expected to grow as CCS technologies scale; the Oil and Gas Climate Initiative (OGCI) estimates that CO₂ utilisation could grow from approximately 250 Mtpa in 2024 to between 430 and 840 Mtpa, driven by expanding demand for synthetic fuels, low-carbon chemicals, building materials and carbon removal pathways.

This creates a growing paradox: decarbonisation may increase industrial dependence on captured CO₂ whilst simultaneously reducing many of the industries that currently supply it.

Following the 2021 fertiliser crisis and subsequent energy-market volatility, concerns surrounding CO2 resilience have increasingly shifted from a niche industrial issue to a broader strategic vulnerability. That shift is also reflected in forecasts for growing UK CO₂ demand.

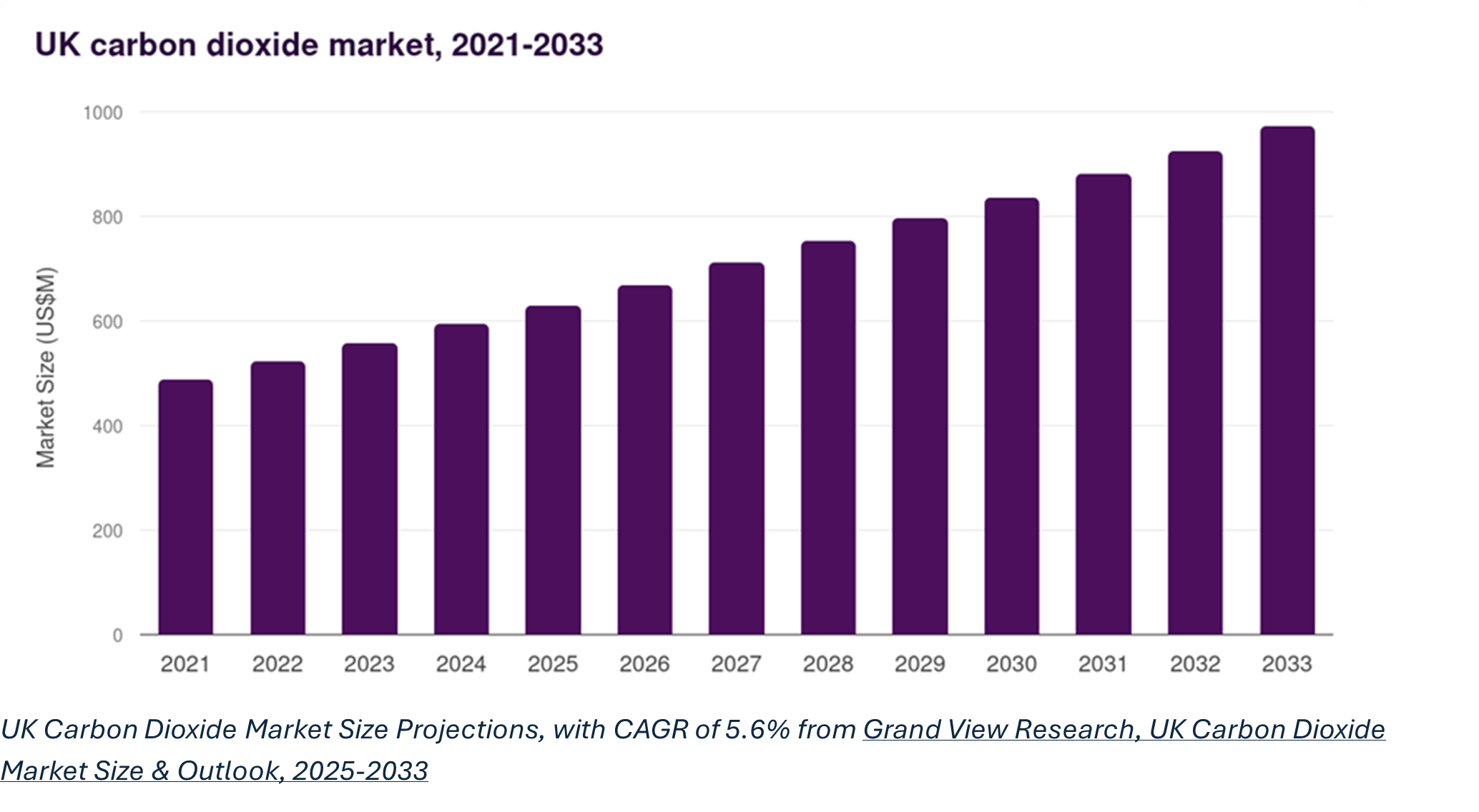

Grand View Research estimated that the carbon dioxide market generated approximately $592.9 million USD in 2024, and could approach $1 billion USD by 2033. Meanwhile, Expert Market Research estimates that UK CO₂ demand could increase from approximately 767,000 tonnes in 2025 to around 899,000 tonnes by 2035.

The UK’s Industrial Exposure

Though not the case globally, food and beverage applications are estimated to account for approximately 72% of UK merchant CO₂ consumption. (https://www.expertmarketresearch.com/reports/united-kingdom-carbon-dioxide-market). Based on projected 2025 demand volumes, this implies the sector alone could require roughly 555,000 tonnes of commercial CO₂ annually.

The scale of UK dependency becomes clearer when examining major manufacturing facilities. Coca-Cola Europacific Partners’ Wakefield site (often described as Europe’s largest soft drinks factory by production volume) operates production lines capable of producing around 2,000 cans per minute, while Britvic’s Beckton facility operates at a similar scale. Beyond food and beverage manufacturing, companies such as Carbon Capture Scotland / Carbon Removers use more than 10,000 tonnes of CO₂ annually for dry ice production, while targeting up to 1 million tonnes of CO₂ removals per year by 2030.

These examples illustrate how deeply commercial CO2 is embedded within manufacturing cold-chain logistics and emerging carbon-management industries.

At the same time, the UK’s domestic CO₂ supply base remains structurally concentrated around a shrinking number of facilities.

Merchant CO₂ availability remains dependent upon the economics of separate industries, particularly fertiliser production, ammonia manufacturing, bioethanol processing and industrial chemical operations. Historically, CF Fertilisers represented one of Britain’s most significant domestic suppliers, with government estimates previously suggesting the company accounted for around 60% of UK commercial CO₂ production.

Alongside fertiliser production, bioethanol facilities have become increasingly important supply hubs. Ensus, located at Wilton on Teesside, currently supplies approximately 250,000 tonnes of biogenic CO₂ annually through bioethanol fermentation. This is potentially equivalent to roughly one-third of UK merchant CO₂ demand.

British Sugar’s Wissington facility similarly produces around 20,000 tonnes of CO₂ annually from bioethanol production, with the captured gas purified and liquefied for use across food, pharmaceutical and chemical markets.

Recent industrial closures, however, have exposed how narrow this domestic supply base has become. In 2025, Associated British Foods announced the closure of the Vivergo bioethanol plant in Hull, reducing domestic supply optionality further and increasing reliance on imports and remaining facilities.

Concerns surrounding CO₂ resilience eventually became serious enough for direct government intervention. Ultimately, the UK government supported a temporary restart of the Ensus facility to help to safeguard domestic CO₂ availability for food systems, healthcare and civil nuclear operations.

The intervention followed disruption across European fertiliser and industrial gas markets linked to gas-price volatility, reduced ammonia production and wider geopolitical instability associated with tensions involving Iran and the Middle East.

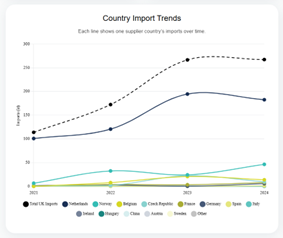

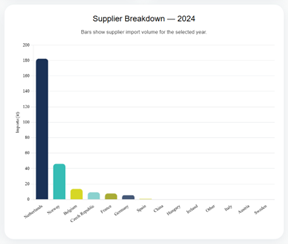

Domestic production, however, only covers part of the picture. Trade data suggests the Netherlands accounts for the most significant proportion of these imports, showing how the UK’s industrial output is propped up against continue stability of wider European energy and manufacturing systems.

This dashboard illustrates how disruption in one part of the industrial system can rapidly cascade into others, transforming what initially appears to be a regional geopolitical issue into a broader industrial resilience challenge.

https://codepen.io/ab_olsights/embed/QwGvjVY?default-tab=result

As industrial sectors face growing volatility, restructuring pressure and transition-related disruption, commercial CO₂ availability may become increasingly unstable. At the same time, demand for captured CO₂ continues to grow across synthetic fuels, low-carbon chemicals and carbon-removal systems.

Britain increasingly treats CO₂ as an emissions problem, while simultaneously depending upon it as a form of critical industrial infrastructure. The Strait of Hormuz disruption ultimately revealed something much larger than a temporary supply-chain concern. It exposed how deeply modern industrial systems, from food security to healthcare resilience, remain dependent on reliable access to commercial CO₂.

Commercial CO₂ is no longer just an emissions issue, it is rapidly becoming a strategic industrial commodity at the centre of the transition economy itself

by Aashna Bhugun Olsights Energy Engineer